When the economy runs hot, Midwest stability is often overlooked for faster-growing regions of the country, but when uncertainty takes hold, the Midwest shines bright. Now, with Sunbelt markets weakening amidst a slowing economy and increasing supply, the Midwest is once again having its well-deserved moment in the sun.

One of the most active Midwest multifamily markets is Indianapolis, so we thought now would be a good time to discuss what’s happening in the Indianapolis MSA. In terms of sales volume, Indiana had the sixth highest sales volume in the country YTD in 2023, according to Cushman & Wakefield. This is not surprising because rent growth in Indianapolis continues to be impressive relative to more well-known multifamily markets in the Sunbelt.

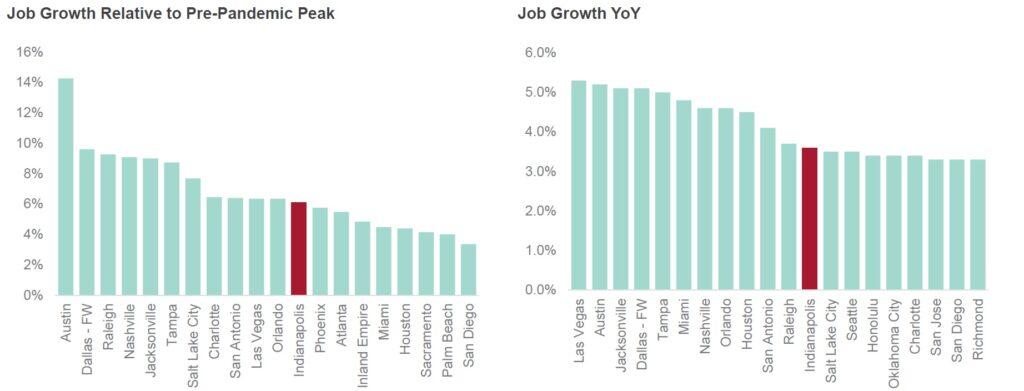

Indianapolis has expanded its employment base by more than 6% since the pandemic began in February 2020, in line with some of the fastest-growing markets in the country. This employment expansion is more robust than even Phoenix, Houston or San Diego. This is a relatively under-appreciated storyline, and it is one of the reasons we like to invest in Midwest markets rather than higher profile Sunbelt markets.

Indianapolis’ Job Growth Has Outperformed

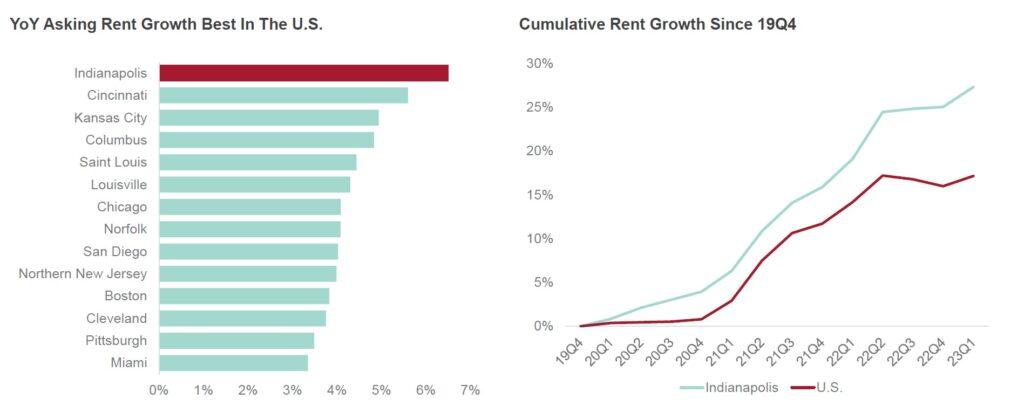

Strong Growth & Minimal Supply Translating To Healthy Indianapolis Rent Growth

Despite Indianapolis’ outsized economic recovery, its off-the-radar nature has helped keep fundamentals relatively sound. Developers have primarily preferred more dynamic metros like Austin and Nashville rather than Indianapolis, which has allowed the Hoosier City to benefit. Since 2019, Indianapolis’ multifamily inventory has expanded by 5.3%, well below the national average of 8.1%. As a result, stabilized vacancies have remained more than 30 basis points below the average since 2010. That out-performance is likely to continue, as Indianapolis has a much smaller construction pipeline than the broader U.S. average and even some other Midwest markets like Columbus and Milwaukee.

These strong fundamentals, combined with a relatively small pipeline of new developments and a fast-growing economy, have pushed asking rent growth in Indianapolis to the top of the national average. Over the past year, rents grew by 6.5%, topping all metros with more than 80,000 units. Some metros may have larger loss-to-lease figures than Indianapolis due to stellar rent growth; however, the performance since the start of the pandemic has been remarkable and under-discussed at a national level.

Indianapolis Rent Growth Has Outperformed

Since the end of 2019, rents are up 27% , well ahead of the national figure. Also evident in the chart is Indianapolis’ relative stability. Across the country, rents cooled in the second half of 2022, but in Indianapolis, rents mostly flatlined, with negligible losses between August and December of last year, with the market resuming outsized growth in January. The key reason – Indianapolis remains one of the most affordable metros in the nation. The market has the 6th lowest rent-to-income ratio in the country, trailing only a handful of other Midwest metros.

Indianapolis Cap Rates Remain Relatively Stable

In terms of cap rates, Midwest markets like Indianapolis have never been known for the boom and bust cycles experienced by Sunbelt markets. In addition, Indianapolis has historically been a higher cap rate market, which reflects lower growth expectations historically. This makes value add investment plans in the Midwest much more straightforward than identical strategies in markets like Phoenix and Houston.

But history looks backward, not forward, and investors are paid to look forward. The growing trend of on-shoring and re-shoring are clearly creating higher rates of job growth in markets like Indianapolis, Cincinnati, Columbus, and even Dayton, Ohio. We love Indianapolis, and we are still experiencing rent growth on rehab trade outs of between 50% and 60% in the southern reaches of the MSA.

Most important, we purchased these assets at a significant discount to where these assets would trade in a market like Phoenix, where job growth is weakening at the same time that record new supply is coming online and rents are weakening. This is leading to negative YOY rent growth in Phoenix, at least for the time being.

In comparison, cap rates in Indianapolis have remained stable, while at the same time new supply is limited, employment growth is expanding, and rents are still growing. Would you rather be invested in Phoenix or in Indianapolis? We think the answer is clear, and we’ve been putting our money where our mouth is since 2006.