CoStar Report Highlights Detroit, Kansas City & Cleveland

Costar is reporting that modest Midwest construction pipelines are limiting supply in the face of steady demand, which is leading to rent growth that is leading the nation.

We have been through multiple cycles in the Midwest, and we know that nothing has changed in our home markets. They are simply chugging along as they always have in response to steady demand for rental housing. What has changed, as usual, is that once hot cyclical markets have entered a downturn.

In fact, rent growth nationwide has slowed significantly since the first quarter of 2022, from 9.9% to just 1.0% for 2024’s fourth quarter. Weakness in national rent growth stems largely from Sun Belt markets, which have experienced significant deceleration amid oversupply.

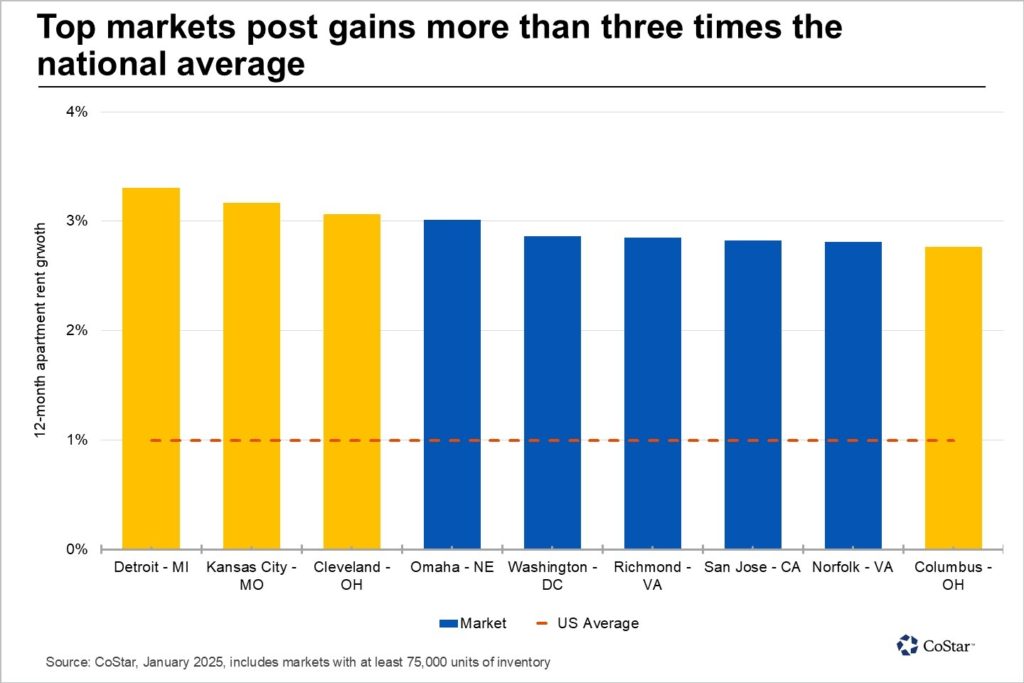

Just like the last downturn in 2009-2010, the metropolitan areas with the most robust rent growth included many “steady eddy” markets in the Midwest, including Detroit, Kansas City, Missouri, and Cleveland and Columbus, Ohio.

Detroit led the country in rent growth in 2024. Apartment rents grew in Detroit by 3.3%, which was an almost 300% increase in 2023 rent growth. CoStar attributes this accelerating growth to above-average demand, which reached a three-year high. In addition, vacancy in Detroit in Detroit decreased from almost 8% to almost 7%.

Midwest affordability relative to other parts of the country is also driving growth in Detroit. The average monthly rent in the Motor City at year end 2024 was $1,320, which is still about 23% below the national average. Rent growth is projected to rise further in 2025 and eclipse 5% by the second half of the year.

The Kansas City multifamily market saw similar improvement in 2024 as demand increased and pressure from new construction began to slow. At the end of 2024, the vacancy rate dropped 90 basis points to 7.9%.

Two Ohio markets, Cleveland and Columbus, round out the list. Apartment rent growth in Cleveland was 3.1% in the final quarter of 2024. Rent growth ended the year 80 basis points ahead of the pre-pandemic average and three times the national average.

Market conditions improved across the Cleveland market in 2024 as absorption improved to 1,600 units. This marked the highest total in three years, as tepid demand in 2022 and 2023 increased the market’s vacancy rate by just over 300 basis points. Meanwhile, completions fell nearly 30% year over year, slowing supply-side pressures.

Although completions will accelerate in Cleveland this year after construction starts hit an all-time high in early 2024, few units have broken ground over the past nine months, which will result in a pullback in completions by 2026. This places downward pressure on the vacancy rate, and CoStar expects rent growth to accelerate in Cleveland over the next 12 to 18 months as market conditions tighten.

Columbus, Ohio’s capital, ended 2024 with an annual growth rate of 2.8%. Apartment demand in 2024 totaled nearly 6,000 units, double the average in the five years preceding the pandemic. Columbus saw a 33% pullback in completions year over year, and demand outpaced supply for the first time since 2021. The result was a 25 basis point drop in vacancy over the past year and steady rent growth.

Tightening market conditions will likely continue in Columbus through 2025 as demand remains above long-term averages and construction activity slows, driving a reacceleration in rent growth in Columbus over the next six to 12 months.