Identifying and Managing Real Estate Investment Risk

Risk is the foundation of economic progress. Without taking risks—or worse, misunderstanding them—you inevitably miss opportunities. The key isn’t to avoid real estate investment risk. It’s to identify, control, and manage it in a way that aligns with your investment objectives.

We view real estate investment risk through two critical lenses: market risk and asset risk.

- Market Risk – the risk driven by macroeconomic cycles and capital flows.

- Asset Risk – the risk driven by specific property-level factors like location, quality, and strategy.

Each of these risks carries its own playbook for control. Understanding how they interact is what separates experienced investors from those who get caught flat-footed when the cycle inevitably turns.

So the question remains simple: How do you control risk when real estate markets are constantly changing? And the answer lies in knowing what risks exist—and building systems to manage them deliberately.

Fortunately, we’ve developed strategies that avoid costly mistakes and allow us stay flexible as markets shift.

Real Estate Investment Risk: Understanding Market Risk

Real estate markets are inherently cyclical. Prices don’t simply move in one direction—they rise, peak, decline, and recover. Recognizing this pattern is essential to managing market risk. When you ignore cycles, the consequences can be catastrophic.

In fact, from 1985 to 1995, falling real estate valuations during the Savings & Loan crisis broke the back of almost 1,000 U.S. banks and thrifts. The federal government had to step in, creating the Resolution Trust Corporation to liquidate over $400 billion in real estate assets from insolvent institutions.

These banks took excessive market risk on real estate, and consequently failed.

A more recent example comes from 2007, right before the global financial crisis.

Sam Zell famously sold Equity Office Properties (EOP) to the Blackstone Group for $39 billion. The EOP portfolio included 573 office buildings, and Blackstone immediately flipped hundreds of less desirable office properties for $27 billion to other buyers.

That moment turned out to be the peak of the last real estate cycle.

Both Zell and Blackstone recognized the market risk—and transferred it to others.

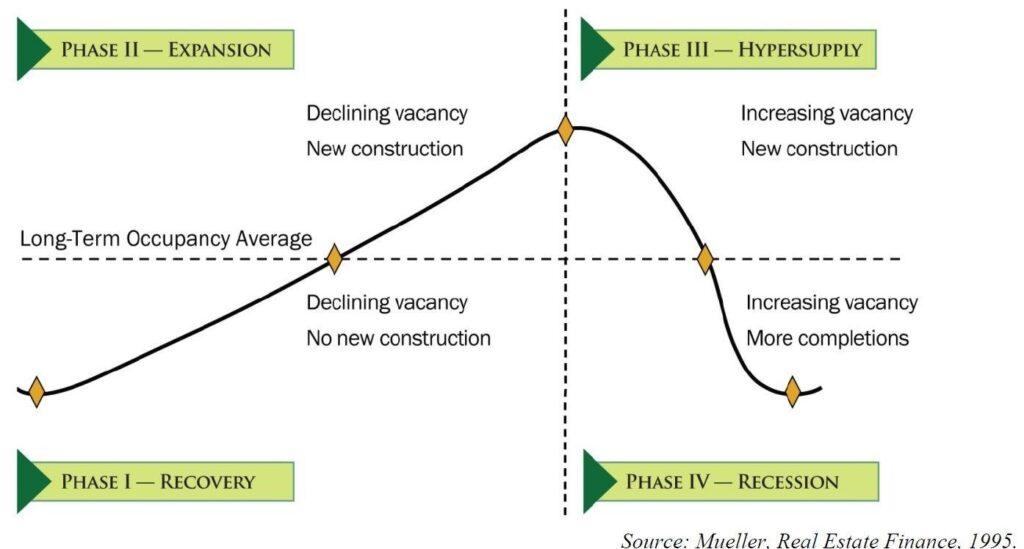

How to Visualize Market Cycles and Risk

One of the best tools for understanding market cycles is the Market Cycle Quadrant, developed by Dr. Glenn Mueller, a prominent researcher and investment strategy consultant for public and private REITS.

It helps investors visualize where the risk lies in different phases of the cycle:

Real Estate Market Cycle Quadrants

Real Estate Market Cycle Quadrant

- Phase I: Recovery – Minimal risk; opportunities abound.

- Phase II: Expansion – Rising prices, but risk starts building.

- Phase III: Hyper Supply – Risk accelerates as supply outpaces demand.

- Phase IV: Recession – Distress peaks, but buying opportunities emerge.

Market risk in Phase I of the quadrant is negligible, but market risk increases as you move into Phase II of the cycle. Investing in Phase III of the cycle entails the most market risk, so in this quadrant it pays to invest in assets & locations you know very well and with experienced sponsors.

Importantly, “hyper supply” relates not just to new construction volume—but also to the availability of capital. When debt and equity flood the market easily, it’s often a sign that risk is peaking. Liquidity surges can mask underlying weakness, while liquidity shortages can create generational buying opportunities.

Investors can make money at any point in the cycle, just as Sam Zell and Blackstone did in Phase III of the cycle in 2007.

Nevertheless, investing in Phase III and Phase IV of the cycle generally requires more agility, knowledge and experience.

Real Estate Investment Risk: Understanding Asset Risk

While market risk affects the broader environment, asset risk drills down to the property level.

It’s the risk tied to the specific asset you’re buying—and managing it well can mean the difference between outperforming or underperforming in any market cycle.

At its core, managing asset risk is about one thing:

Buying below intrinsic value and conducting thorough due diligence before closing.

If you misprice the asset—or miss red flags during diligence—no amount of market growth can save you. Conversely, if you control asset-level risks properly, you can create value in any phase of the market cycle.

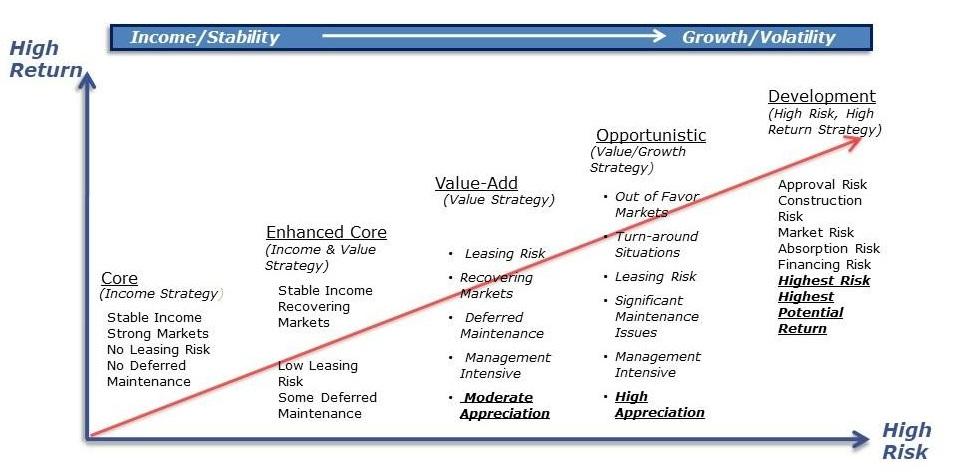

How to Visualize Asset Risk

Think about asset risk through the lens of this Risk-Return Graph. Lower risk strategies generate lower returns, while the more risky strategies like value-add and development carry higher returns:

Value Add & Development Are Generally Higher Risk Strategies

Real Estate Risk-Return Spectrum

- Core Assets:

- Trophy properties in prime locations.

- Lowest risk, but lowest returns.

- Value-Add Assets:

- Properties needing repositioning, renovation, or management improvements.

- Higher risk, but higher return potential.

- Development Projects:

- New construction or heavy redevelopment.

- Highest risk—and highest potential upside.

Each step up the return curve requires accepting more uncertainty. Development, for example, carries risks around approvals, timelines, construction costs, labor shortages, and access to capital—all factors largely outside the developer’s control.

Navigating Asset Risk Through Market Cycles

In times of turbulence, investors naturally migrate toward Core assets to minimize exposure.

We saw this clearly during the 2008 financial crisis when institutional capital crowded into New York, Los Angeles, and other gateway cities. However, that flight to safety created mispricing’s elsewhere. It left compelling value-add and opportunistic deals overlooked in secondary markets.

At Piping Rock, we don’t shy away from these periods of dislocation. In fact, two of our best-performing investments were acquired during Phase III and Phase IV of the market cycle—precisely when others were retreating.

It’s proof that you can succeed in any phase—if you understand both market risk and asset risk, and invest accordingly.

If you want to learn more about our real estate investment strategy, click here.